WASHINGTON (RNS) — The Rev. Melech E.M. Thomas attended two seminaries and graduated from the second, a historically Black theological school, in 2016.

That academic journey has put him in the pulpit of an African Methodist Episcopal Church in North Carolina.

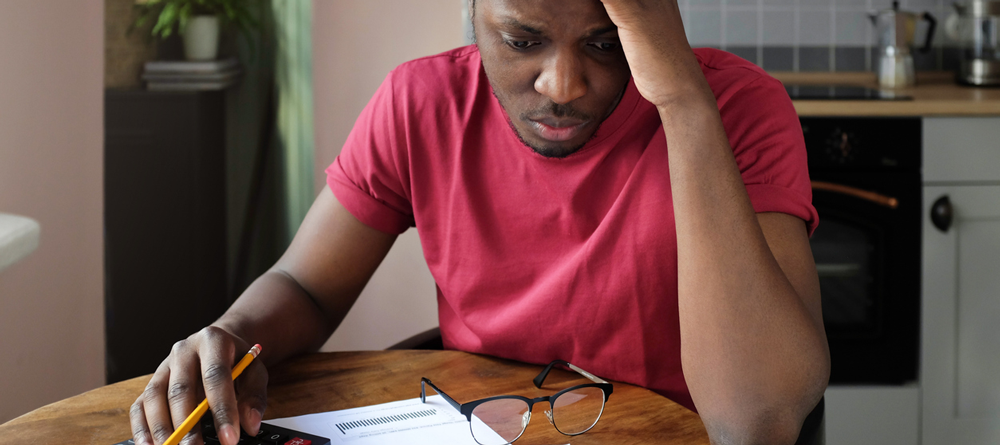

But his pursuit of a Master of Divinity degree also left him about $80,000 in debt.

“The tuition was less, but I still had to live,” he said, describing other seminary-related costs after his transfer from Princeton Theological Seminary to the Samuel DeWitt Proctor School of Theology at Virginia Union University. “I’m in seminary full time. And I got to make sure I’m paying rent, that I’m eating, all those other expenses.”

Thomas traveled to the nation’s capital in early February for a meeting with other graduates, leaders and students of Black theological schools to discuss possible solutions for the disproportionately high debt of Black seminarians.

Delores Brisbon, leader of the Gift of Black Theological Education & Black Church Collaborative, said it’s important for leaders to understand the sacrifices being made by students who pursue seminary degrees in historically Black settings.

“We need to address this issue of debt,” she said, opening the collaborative’s two-day event, “and determine what we’re going to do about it.”

According to data from the Association of Theological Schools, debt incurred by Black graduates in the 2019-2020 academic year averaged $42,700, compared with $31,200 for white grads.

Data shows 30% of Black graduates in the 2020-2021 academic year had debt of $40,000 or more, compared with 11% of white graduates.

Thomas, 34, said his debt, necessary to achieve his degree and gain ordination, has led to a church appointment that “pays me enough to pay rent,” but not his other living expenses. Yet, Thomas said he knows he’s in a better situation than some other graduates of historically Black seminaries.

“I’m grateful,” he said. “But it’s extremely tough.”

The collaborative includes five Black theological schools — Hood Theological Seminary, Interdenominational Theological Center, Payne Theological Seminary, Samuel DeWitt Proctor School of Theology and Shaw University Divinity School. Lilly Endowment Inc. has given three grants between 2014 and 2020 totaling $2.75 million to the In Trust Center for Theological Schools to help facilitate coordination and increased mutual support between the schools, including the recent meeting about student debt.

The Rev. Jo Ann Deasy, co-author of a 2021 report on the ATS Black Student Debt Project, told the dozens gathered at a Washington hotel that the project came about as researchers discovered how “Black students were just burdened by debt more than any others.”

She said ATS is seeking to help change perceptions about what the project calls the “financial ecology of Black students” as seminarians seek training to become religious leaders, churches hope to hire them and theological institutions consider expanding financial networks to aid them.

“We’re trying to help people shift their understanding of finances from really individual responsibility to a broader systemic understanding of how finances operate in our communities and in our churches,” she said. “This is just a part of that shift toward understanding that it’s not the students’ fault but that this is a bigger issue that we need to address together.”

The report described “money autobiographies” of students who sought financially stable circumstances as they attended theological schools, whether historically Black, white or multiracial.

“They noted the disparities in financial support, particularly from congregations and denominations, between themselves and their White colleagues, a disparity that was often not seen or acknowledged by their peers or the institutions they attended,” the report states.

The average annual tuition for an M.Div. — before any scholarships are considered — is $13,100 for free-standing Protestant schools and $12,500 for Protestant schools related to a college or university. Chris Meinzer, senior director and COO of ATS, said that, on average, it takes students about four years to complete an M.Div. degree.

Seminary graduates who attended the Washington event spoke of having few scholarship options and having to take out loans to pay for expenses including or beyond tuition.

“It’s the cost of being enrolled and the cost of student fees along with your books,” said the Rev. Jamar Boyd II, senior manager of organizational impact at the Samuel DeWitt Proctor Conference, which supports African American ministries. Depending on the class and the number of books required, it could amount to as much as $600 to $700 in a semester, said Boyd, 27, a graduate of Virginia Union University’s theological school.

“If you’re a full-time student taking three or four classes, that’s a paycheck,” he said.

Minister Kathlene Judd, a theologian in residence at an Evangelical Lutheran Church in America congregation in North Carolina, said she eventually chose debt over the mental stress of working, studying and supporting a family at the same time.

She worked in information technology as she went through seminary and continues that career as she pays off her debts after originally hoping to pay for seminary without taking out loans.

“If I’m being fully transparent, I had no idea what I was getting myself into,” said Judd, 38, who graduated from Shaw University Divinity School in 2020.

She said it was a “big decision” to borrow money to continue the education she felt God called her to pursue.

“But honestly, it came down to my mental and emotional health,” she said.

Many students and grads, like Judd, are at least bivocational.

The Rev. Lawrence Ganzy Jr. is in his fourth year at Hood Theological Seminary, where he attends a track that allows him to pastor an African Methodist Episcopal Zion Church in South Carolina while taking classes on Friday nights and Saturdays. During the week, he’s an admissions officer for Strayer University.

Prior to seminary, his work through the Carolina College Advising Corps, a government program for University of North Carolina-Chapel Hill graduates to counsel low-income high school students, helped him afford the start of his theological studies.

“That paid for my first year of seminary,” said Ganzy, 26. “Then when I got to the next year, that money was gone.”

Keynoting the opening night of the collaborative meeting, the Rev. Michael Brown, president of Payne Theological Seminary in Wilberforce, Ohio, pointed to the portion of the Lord’s Prayer that says “forgive us our debts as we forgive those who are indebted to us” in the Gospel of Matthew.

“Debt keeps us chained to the past and it doesn’t open up possibilities for the future,” he said, “and so the idea of the forgiveness of debt in the Lord’s Prayer is that it releases you to do things for God.”

During the event, graduates spoke of the additional financial struggles they faced, such as debt affecting their credit scores as they try to purchase a car and escalating rent, sometimes in historically Black neighborhoods that have been gentrified.

Brisbon pointed out that Black theological schools may have small endowments and may not get support from their alumni, in part because of the often-lower salaries received by their graduates.

“Black preachers may love their school as much as somebody else but they can’t give money that they don’t have,” she said.

The ATS report noted that a 2003 Pulpit & Pew study found that, on average, Black clergy salaries were about two-thirds those of white clergy. In a 2019 Christian Century essay, scholars noted that a study by the Samuel DeWitt Proctor Conference found that one-third of Black pastors believed they were “fairly and adequately compensated as a professional” while 67% said that they had “particular financial stress” at that current time.

The Rev. Leo Whitaker, executive minister of the Baptist General Convention of Virginia, told Religion News Service that some clergy in the more than 1,000 churches in his Black state denomination are often “bivocational if not trivocational” to make ends meet, especially when they are located in a region like the state’s Northern Neck rather than the city of Richmond.

Whitaker suggested to collaborative members that they look to U.S. government programs that offer debt forgiveness to educators and doctors who serve in needy communities, noting they should offer the same for seminary grads. He hopes collaborative members will discuss his idea with seminary and education officials.

“You’re serving a stressed community and you’re financially stressed yourself without the ability to make the necessary funds and it’s not about them having a choice of where they choose to serve,” he said, noting that Methodist bishops appoint clergy and Baptist clergy go where congregations have called them to serve. “In ministry our location is not always assigned to us by choice.”

Bishop Teresa Jefferson-Snorton of the Christian Methodist Episcopal Church, a historic Black denomination, said laypeople and clergy may not be aware of the sacrifices made by seminarians and recent graduates as they pay seminary tuition that is far more than what she paid 40 years ago.

“Most of our highly organized denominations don’t really have a grasp on what they are actually doing or not doing to support theological education,” Jefferson-Snorton added. “Although in many cases we promote it, we encourage it. But we don’t resource it and I think that needs to be brought to the attention of the church.”

RNS receives funding from Lilly Endowment Inc. RNS is solely responsible for this content.

The leaders of Pathway Church on the outskirts of Wichita, Kan., had no clue that the $22,000 they already had on hand for Easter would have such impact.

The nondenominational suburban congregation of about 3,800 had set out only to help people nearby pay off some medical debt, recalled Larry Wren, Pathway’s executive pastor. After all, the core membership at Pathway’s three sites consists of middle-income families with school-age kids, not high-dollar philanthropists.

But then they learned that, like a modern-day loaves-and-fishes story, that smaller amount could wipe out $2.2 million in debt not only for the Wichita area but all available debt for every Kansan facing imminent insolvency because of medical expenses they couldn’t afford to pay — 1,600 people in all.

As Wren thought about the message of Easter, things clicked. “Being able to do this provides an opportunity to illustrate what it means to have a debt paid that they could never pay themselves,” he said. “It just was a great fit.”

Churches in Maryland, Illinois, Virginia, Texas and elsewhere have been reaching the same conclusion. RIP Medical Debt, a nonprofit organization based in Rye, N.Y., that arranges such debt payoffs, reports a recent surge in participation from primarily Christian places of worship. Eighteen have worked with RIP in the past year and a half, said Scott Patton, the nonprofit’s director of development. More churches are joining in as word spreads.

The mountain of bills they are trying to clear is high. Medical debt contributes to two-thirds of bankruptcies, according to the American Journal of Public Health. And a 2018 Kaiser Family Foundation/New York Times poll showed that of the 26% of people who reported problems paying medical bills, 59% reported a major life impact, such as taking an extra job, cutting other household spending or using up savings. (Kaiser Health News is an editorially independent program of the foundation.)

The federal Consumer Financial Protection Bureau proposed a rule last month to curb debt collectors’ ability to bug those with outstanding bills, and some states have tried various measures, such as limiting the interest rates collectors may charge. But until a comprehensive solution emerges, churches and others are trying to ease some of the load by jumping into the debt market.

A big part of RIP’s appeal comes from the impact even a small donation can have, say participating church leaders. When a person can’t pay a bill, that debt is often packaged with other people’s debt and sold to bill collectors for some fraction of the total amount of the bill. Those debts usually come from low-income people and are more difficult to collect.

RIP Medical Debt buys debt portfolios on this secondary market for pennies on the dollar with money from its donors. But instead of collecting the debt, RIP forgives it.

To be eligible for repayment from RIP, the debtor must be earning less than twice the federal poverty level (about $25,000 a year for an individual), have debts that are 5% or more of their annual income and have more debt than assets.

Because hospitals and doctors are eager to get those hard-to-collect debts off their books, they sell them cheap. That’s how, Patton said, those 18 churches have been able to abolish $34.4 million of debt since the start of 2018.

Working this way puts a high-dollar project within reach of even small churches. Revolution Annapolis, a nondenominational Maryland church with Sunday attendance of around 200 and without a permanent building, wiped out $1.9 million in debt for 900 families in March. Total amount raised: $15,000.

Revolution leaders heard about RIP Medical Debt on a segment of John Oliver’s “Last Week Tonight” in 2016, said Kenny Camacho, lead pastor. But at the time, they didn’t think they had the resources to make much of a splash.

After hearing about another church that paid off millions last year, Revolution leaders decided to try it. At most, they hoped to have an impact in their area, Camacho said. But the money went much further, eventually covering 14 counties in eastern and central Maryland.

Emmanuel Memorial Episcopal Church, a congregation of about 175 families in Champaign, Ill., had a similar experience. The original idea was to try to have an impact just in Champaign County, said the Rev. Christine Hopkins. But their $15,000 abolished $4 million of debt for the entire diocese, which stretches across the southern half of the state.

“We were bowled over, actually,” Hopkins said. “It was to the point of tears.”

In many cases, churches have not had to do a fundraising campaign because their contribution came from money already on hand. Emmanuel Episcopal, for instance, had leftovers from a campaign set up a year ago to celebrate the centennial of its church building.

The Fincastle Baptist Church, with 1,600 members in the Roanoke, Va., area used money it had budgeted for an annual “Freedom Fest” event to honor first responders, and then partnered with local television station WSLS in a telethon to raise more. That effort abolished over $2.7 million in medical debt targeted at veterans.

The RIP nonprofit allows donors to choose geographic areas they want to reach and can pinpoint veterans as recipients. But beyond that, no restrictions are allowed, Patton said. A church can’t specify which types of medical procedures could be paid for or anything about the background of the recipients.

That didn’t bother church leaders contacted for this story. But it is a subject that’s been broached by donors of all types in the past, Patton said.

For instance, some potential donors have asked to exclude people from different faiths or certain political parties, he said. “It’s just absurd. This is not a revenge tactic,” Patton said. “People who are requesting those things really don’t understand philanthropy.”

Churches don’t necessarily experience a direct return in the way of new members. All the processing goes through RIP Medical Debt, which sends letters notifying the beneficiaries their debts have been forgiven. Donors can have their names listed on those letters, but not everyone opts to do so.

New membership wasn’t the point for Pathway Church in Kansas, Wren said. “Sometimes the more powerful spiritual message is when you’re able to do something for somebody that you’ll never meet.”

The Revolution Church decided against putting its name on the notification letters, Camacho said, because it didn’t want beneficiaries to feel obligated. “When a person has their debt forgiven, we want them to experience that as a kind of no-strings-attached gift,” he said. “We don’t want there to be any sense that because we did this now they should visit our church or something.”

Besides, he said, the gift covered an area large enough that some beneficiaries live a couple of hours away. “I would much rather them think more positively about the church down the street from where they live.”

Donors sometimes hear back from the people whose debts they’ve paid, but not often. Many don’t expect it. “I guess that’s a biblical story, too. Jesus forgave 10, and only one said thank you,” Hopkins said.

Churches have a lot of choices when it comes to charity, but medical debt and affordability issues often resonate with parishioners. Some churches are worried enough about medical costs for their members that they subscribe to cost-sharing nonprofits, in which members pay each other’s medical bills.

Medical mission work has long been an important form of outreach for Fincastle Baptist Church in Virginia, said associate pastor Warren King. The church runs a free clinic, and mission trips to other countries usually include a medical component.

Paying off medical debt is an extension of that line of thinking. “We need to do not just this thing but many things that practically show the love of God,” King said. “It’s hard to tell somebody God loves you if they’re starving and you don’t try to deal with the problem.”

Hopkins said the debt outreach was a satisfying project for her Illinois congregation because it could resolve a problem for the beneficiaries. “We do a lot of outreach that’s food-related and housing-related. This was something different,” Hopkins said. “You help feed somebody, and you’re feeding them again the next day. This was something that could make an impact.”

Purchasing a home is one of the biggest decisions a person will make. The process can be exciting, and equally daunting. But ultimately it’s a step toward fulfilling the American Dream.

In the wake of the current economic downturn, however, the notion of homeownership seems less attainable than before. And for many current homeowners, the threat of foreclosure has turned the American Dream into a nightmare. Hundreds of thousands of families each year are now faced with the reality of losing their homes due to high interest rates and subprime lending, and the crisis has hit the African American community especially hard.

Last year, a Pew Research Center study revealed that wealth among black Americans dropped 53 percent during the current recession as the result of falling home prices. What’s more, black homeownership rates fell to the lowest level in 16 years.

One company working to reverse these trends is HomeFree-USA, which has been a leader in bringing awareness to the foreclosure discussion in the black community.

Marcia J. Griffin

“Our mission is to provide both information and inspiration,” says HomeFree-USA president and founder Marcia J. Griffin. “We try to teach families and individuals that there are things they can do to improve their situations and avoid foreclosures.”

As a HUD-approved non-profit organization, Griffin’s organization has been aiding families across America in securing and maintaining their dreams of homeownership. According to Griffin, HomeFree-USA has helped more than 7,000 families since 1995, and not one of them has gone into foreclosure.

On Saturday July 21 in Chicago, HomeFree-USA will host “Homeownership for All,” a free community seminar designed to educate and encourage people interested in gaining more insight about buying or keeping a home, all while living debt free.

Joining Griffin and her team of experts will be the Rev. DeForest Soaries, senior pastor of First Baptist Church of Lincoln Gardens in Somerset, New Jersey, and the author of dfree: Breaking Free of Financial Slavery. Soaries, who will share spiritual principles for successful money management, brings years of practical experience on issues related to the black family. He formerly served as New Jersey’s Secretary of State and was featured in the CNN documentary Almighty Debt

“We think it’s imperative that churches and faith-based organizations be leaders in teaching their communities about financial literacy,” says Griffin. “No one has been giving us wise advice on these matters, so faith-based organizations have an opportunity to make a difference.”

Griffin, who as one of 19 HUD intermediaries in the nation is able to bring both informational and financial assistance to local communities, plans to take the “Homeownership for All” seminar to other cities as well. Following the Chicago event, HomeFree-USA plans to make stops in Detroit, Washington D.C., Miami, and Atlanta.

With high expectations for the Chicago meeting, Griffin says that her hopes are to have a full house. “We certainly want a packed house, with about 200 people determined to make their financial situation better,” she says.

For more information about HomeFree-USA and its upcoming events, call 301-891-8400 or go to HomeFreeUSA.org.

POINT/COUNTERPOINT: Protesters from either side of the political divide have descended on Washington this year to make their cases for the preservation or elimination of federal programs.

I have to ask myself: am I part of the American majority who wants to scale back government expenses — as long as none of my personal benefits are touched?

I confess: I turned 63 last week, and I don’t want Social Security or Medicare reduced or — heaven help us — privatized.

I have personal reasons.

My husband and I have been saving heavily for 20 years, have paid off the mortgage on our modest house, have nursing-home insurance policies, and have no debts whatsoever. Nevertheless, our retirement accounts have been significantly diminished by the recession of 2008-11, and the future of stocks and bonds does not look good. Without Social Security to supplement our savings, we’d have a rough retirement.

Both of us take good care of our health. We’ve never smoked, and we exercise daily. We eat no red meat, few desserts, and lots of whole grains, vegetables, and fruit. My weight has always been right where it’s supposed to be, and his isn’t far off. Nevertheless, I’m scheduled to have open heart surgery next week, and I will need to have costly check-ups and possibly medications for the rest of my life. Without Medicare, I’d probably have a very short retirement.

So yes, I’d much prefer that we strengthen Social Security, Medicare, and our entire health-care system and stop paying for 46.5 percent of global military spending, for example.

But my reasons are not entirely personal. Although my husband and I are the kind of people Republicans love (and Jesus worried about), we will be in trouble if the senior safety nets come down, right along with people who have had to face unemployment, divorce, foreclosure, addictions, natural disasters, accidents, disabilities, and catastrophic illness; right along with people who don’t know how to manage money, who abuse their health, and who long ago stopped thinking about tomorrow (see my personal blog for an earlier post, “The United States of Florida“).

Really, folks, this isn’t a question of deserving. As Jesus pointed out, God “makes his sun rise on the evil and on the good, and sends rain on the righteous and on the unrighteous” (Matthew 5:45). God may or may not be the sender, but I’ve noticed that crap falls on both the good and the bad as well. We all benefit from God’s grace, and we’re all just one step away from catastrophe.

Government programs can’t give us comfortable lifestyles if we have no job and no savings. They may not be able to give us good health if our bodies are faulty or abused. They can’t keep us from getting old and dying. What they can do is help us — all of us who need help — have food, shelter, and necessary medical care.

By the way, I’m not saying that Social Security and Medicare are our most important social programs. Nothing is more important than educating our young, and comparative test scores show that the U.S. is in trouble here (22nd place in math!). Still, many of our suburban schools are excellent. We say we believe in equality of opportunity: what are we doing to assure that all of our children, no matter where they live or how much their parents pay in property tax, have access to good schools?

Back to my main point. If all of this means additional funding — a payroll tax on all earned income, for example, and not just the first $106,800 — so be it. If it means ending President Obama’s extremely unwise payroll tax holiday, so be it. If it means I have to pay more taxes, so be it.

Our government is not only of the people and by the people, it is also for the people. May Lincoln’s vision of a nation dedicated to the common good not perish from the earth.

Purchasing a home is one of the biggest decisions a person will make. The process can be exciting, and equally daunting. But ultimately it’s a step toward fulfilling the American Dream.

Purchasing a home is one of the biggest decisions a person will make. The process can be exciting, and equally daunting. But ultimately it’s a step toward fulfilling the American Dream.